Many Canadian tax-exempt investors invest in US equities through a standard Canadian pooled fund. This means that they pay the 15% US dividend withholding tax on US equity investments. This can be refunded.

To illustrate, assume that a Canadian charity invests in Apple stock through a standard Canadian pooled fund. When the dividend is issued by Apple to the pooled fund, the 15% US dividend withholding tax is collected by the pooled fund and sent to the US Internal Revenue Service (“IRS”). However, the charity itself is exempt from the US tax. That means that the charity can claim a refund. Over a three-year period, the amount of withholding tax paid to the IRS may amount to tens of thousands of dollars or more. The legal fees to pursue a refund for the 15% US dividend withholding tax are contingent on the refund being issued. There are no financial or tax risks to the charity in pursuing the refund. This is because the charity has already paid the US tax through the pooled fund and there are no legal fees unless they get a cheque from the IRS. The balance of this article explains the opportunity further.

Which Investors are Eligible for a Refund

Generally, Canadian tax-exempt organizations are able to get a refund for the 15% US dividend withholding tax they have paid even if they invest through pooled funds. Canadian tax-exempt organizations include:

- Indigenous investment trusts

- Foundations

- Churches

- Universities

- Charitable organizations

- Employee benefit plans

- Pension funds

- Municipalities

- Certain not for profit corporations.

Basics of the Dividend Withholding Tax

Under the Canada-US Tax Treaty (“Treaty”), all Canadian resident individuals, corporations or trusts are exempt from US tax on interest income from US sources and capital gains on the sale of US stocks. However, Canadian resident trusts have to pay the 15% US dividend withholding tax on dividends from US stocks unless they are comprised solely of a narrow class of tax-exempt investors.

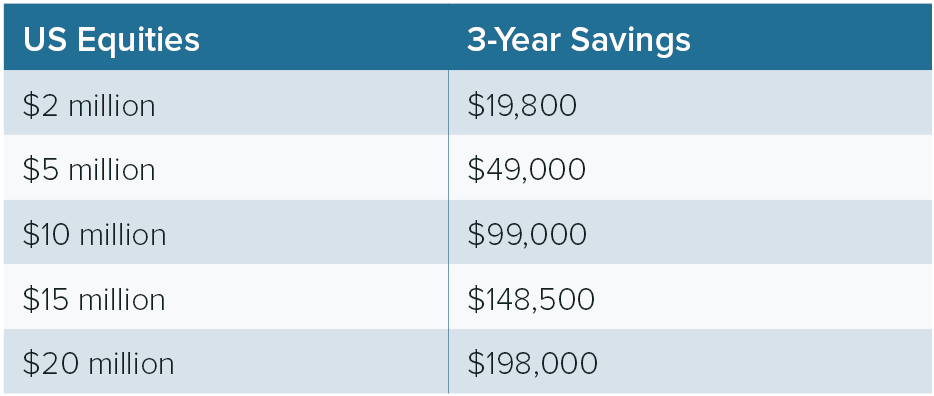

The standard dividend yield in the S & P 500 is 2.2% of the money invested. Of that, 15% is withheld in US taxes. That means that on a yearly basis the dividend withholding tax represents about a 33-basis point cost on the total dollar amount invested in US equities. On a large portfolio this can add up. The chart below illustrates the potential recovery over three years based on amounts invested in US equities.

Even for small portfolios, this is a material amount of money.

Refund Claims

For both US and Canadian tax purposes the US dividend withholding tax (although collected and remitted by the fund itself) is allocated to the investor and thus considered paid by the investor. Since the investor does not owe the tax, with the proper documentation it can apply for a refund for the tax paid. The US tax rules allow for refund claims going back three years.

Polaris Tax Counsel has helped 10 Canadian tax-exempt organizations / entities recover the 15% US withholding tax through their pooled fund investments. Over CAD $ 1 million in US taxes paid has been recovered. Successful clients include pension plans, charities, foundations and Indigenous investment trusts.

Conclusion

Many Canadian tax-exempt organizations invest in US equities through pooled funds and thus pay the 15% US dividend withholding tax. They can get a refund of this tax for the prior 3 years which may amount to tens of thousands of dollars. There are no risks to pursuing these claims because the tax has already been paid and there are no legal fees unless the money is recovered.